Collection period under the loan agreement. Common misconceptions related to loan statutes of limitations

Do banks forgive debts?

Do banks forgive debts? The possibility of widespread consumer lending has allowed people to buy household appliances, clothing, furniture, electronics and other everyday goods on credit at breakneck speed. The promise of repayment of borrowed funds is supported by data on registration, place of work, availability of valuable property, real estate or car.

In the absence of payments, the creditor has the right to bring a claim by going to court. In his demand, he will set out a claim for the recovery of unpaid funds in the manner prescribed by the legislation of the Russian Federation. The Civil Code determines the limitation period for a loan to be three years. The countdown of this period begins from the moment of violation of the rights of the creditor. However, very often disputes arise around the start date of the statute of limitations. There are many nuances, special moments and compromises here.

A clear framework has been established for the regulation of civil disputes - 3 years. This is stated in Art. 200 Civil Code of the Russian Federation.

Based on the dates specified in the contract, in most cases it is not difficult to determine the statute of limitations. Knowing the date of the loan, the expected payment period and the end of the contract, the client can calculate the moment of termination of his obligations. But here we need compelling reasons, and proven ones, otherwise the court decision will not be in his favor. Criminal liability may also be added to the imposition of fines, mandatory payments and possible confiscation of property.

Additional loan obligations - penalties, interest, fines - must be paid along with the main debt. The date of their accrual does not affect this aspect in any way. Even if they entered the general account later or in the last days.

When is a loan invalidated?

The absence of a specified statute of limitations means a “default” procedure, when 90 days are added to the date of the last payment, and three years are counted from it. If the defaulter manages to hide from the authorities and the creditor all this time, then the debt is canceled. The mentioned three months of absence of mandatory contributions give the bank the full right to demand repayment of the full amount through the court, and immediately. This is quite justified, because it turns out that the agreement was violated. Then the person or organization that provided the loan completely terminates all relations with the defendant and obliges him to repay the money in full.

As for the complete absence of a violator of obligations, there are some nuances that make it possible to expose him or “catch him red-handed.” He may, without knowing it, confess, appear red-handed, or otherwise recognize his debt as valid. The statute of limitations is interrupted if the borrower has taken the following actions:

- paying even a small part of the debt - paying even the smallest amount indicates a desire to conscientiously deal with the obligations undertaken;

- signing at least one document that is in any way related to the borrowed money - this will be an official opportunity to prove something in court, the bank can operate on this fact with complete confidence;

- voluntary recognition of oneself as a debtor is an official statement that can be confirmed by witnesses and the defendant himself.

If in a lawsuit the applicant indicates a deadline for fulfilling the requirement, then the statute of limitations will be calculated from the moment of its expiration.

Additional loan obligations

You should not fully rely on the 3 years prescribed in the Civil Code. The fact is that the expiration of the statute of limitations does not necessarily serve as an obstacle to filing a claim for the return of the debt to the creditor (Civil Code of the Russian Federation, Art. 199, Part 1). The court will accept such a claim, and in the vast majority of cases, positive decisions are made on them. They can be challenged by means of an appeal demanding recognition of the expiration of the statute of limitations. True, a smarter and more justified move would be to make such a statement during the trial.

The borrower is in a strong position if he has documentary evidence of his financial or physical insolvency. But still, sometimes a creditor is able to achieve a judicial refusal to recognize the validity of the statute of limitations. The reasons here may be as follows:

- Applying to the court with a request to assist in the process of debt repayment before the expiration of the specified period. It is noteworthy that the trial itself may be postponed indefinitely.

- If work was carried out with debt. This refers to out-of-court settlement measures: telephone conversations or official letters to the borrower. In the first case, audio recordings with the debtor’s voice, made with his knowledge and necessarily containing an acknowledgment of the debt, have evidentiary weight. In the case of letters, it is necessary to prove the personal receipt of the notification by the citizen. The easiest way to confirm this fact is by courier delivery service or registered letters with notification of receipt.

In any case, the maximum period can never exceed 10 years.

The line between lack of solvency and fraud

If the borrower is truly conscientious, and the reasons for financial troubles were health problems, work problems or other proven incidents, it will be possible to avoid payments legally. But the deliberate use of the statute of limitations as a reason to write off a debt borders on. The consequences can be much more serious than the debtor initially expected.

To begin with, if difficult situations arise, you must notify the bank about the temporary impossibility of making mandatory payments. Also, the absence of malicious intent can be confirmed by the following facts:

- collateral for a loan - this can be a salvation if, for example, you re-mortgage a property;

- there are already several payments;

- insignificant debt balance - not too large amount of unpaid loan (less than 1.5 million rubles).

However, even a borrower who is completely acquitted by the court after the statute of limitations has expired is not immune from negative consequences in the form of a damaged credit history.

What should a borrower do if his credit institution is declared bankrupt?

When does the statute of limitations on a loan begin?

Here it is worth paying attention not to the liquidation of the bank itself, but to the suspension of the activities of the credit organization that dominates it.

If absolutely the entire company is liquidated, then the debt is automatically written off, but this happens extremely rarely. We can say that such a possibility is practically excluded.

In fact, work with debt does not stop, even for clients of a bankrupt bank.

Over time, one way or another, the legal successor of the credit institution is determined, so there will definitely be someone who will put all financial affairs in order and find borrowed funds.

How to stop constant reminders about a written off debt?

No bank will just give up its money. After all, if an organization checks the client so carefully before drawing up a contract, persuades them to take out insurance, and then looks for a negligent client, it is unlikely that if they deviate from payments and the statute of limitations expires, they will calm down and write off the entire amount.

The bank can remind you about remaining payments ad infinitum; it is not formally prohibited from doing so. Even if the debtor wins the litigation, but the plaintiff still does not calm down, there is a way to get rid of constant annoying alerts.

Before drawing up a loan agreement, any borrower signs a paper indicating consent to the processing of personal data. Without it, the bank has no right to work with his passport, other documents, call work, or even send SMS messages.

You can revoke this permission, which is done very simply by writing a corresponding application at one of the bank’s offices, which it simply cannot refuse to accept. Now he has no right to even send advertising messages and emails.

At what point does the statute of limitations on a loan begin in the following video:

May 17, 2018 Help manual

You can ask any question below

The statute of limitations on a loan is a very relevant issue at the moment. Many people can often face certain financial difficulties, and therefore this issue is relevant. For example, a person, due to crisis circumstances, suffers losses and cannot return the loan funds, or the bank’s license was temporarily revoked. Below in the article we will look at what to do if the statute of limitations has expired.

What is important to know about the statute of limitations?

A person who has taken out a loan needs to remember some nuances that may be useful. The agreement between the bank and the client states that loan funds are provided subject to mandatory repayment. Based on this, the borrower remains credit obligations until the expiration of the period specified in the relevant document.

That is, in this case, we are not talking about the time during which the borrower must repay the debt, but about the period within which the bank can collect the loan and the interest due on it, as well as other charges in court.

The current legislation of the Russian Federation has a provision under which a financial organization does not have the right to demand fulfillment of obligations that were assigned to the debtor. These provisions include the expired statute of limitations on the loan.

How long can a loan be required to be repaid?

The period for collecting loan funds from the debtor is three years. Moreover, this period begins from the first violations of the conditions on the part of the debtor. This provision is regulated in accordance with Part 1 of Art. 200 of the Civil Code of the Russian Federation. In addition, regardless of when fines for violation of the loan agreement were accrued, their statute of limitations will expire simultaneously with the main debt.

If the loan agreement does not specify the period for debt collection, then it will begin to be calculated from the last late payment. If payments are not received within 3 months (90 days), the financial institution may demand from the debtor the return of the entire amount that was specified in the contract. If such a situation arises, the period will be calculated from the moment this requirement is put forward by the financial organization.

It is worth knowing that even if the statute of limitations on the loan has expired, this does not mean that the financial organization cannot file a claim with the relevant authorities and demand repayment of the debt. In addition, in half of the cases the court may make a decision not in favor of the debtor. You can challenge the claim by filing an appeal with the judicial authorities, citing Article 200 of the Civil Code “On the expiration of the period for collecting loan funds.”

But even despite the fact that the borrower counters with legislative provisions, in some cases financial organizations can seek a refusal through the court.

The reason for this may be:

- The financial organization submits a statement of claim to the relevant authorities before the statute of limitations on the loan expires.

- Carrying out work to fulfill contractual obligations.

In the latter case, the creditor can try to resolve the issue out of court using the following methods::

- Send an official letter to the citizen. However, in this case it must be proven that the letter was received by the borrower.

- When recording a telephone conversation with the borrower admitting his own debt. In this case, the recording should be made only after notification and consent of the borrower.

But the debtor can also help extend the collection period. That is, the statute of limitations will be extended if:

- The citizen signed documents related to appealing the loan debt.

- Part of the loan has been paid (even if this amount is minimal).

- The citizen himself admitted that he was a debtor to the financial organization.

If at least one of the above circumstances occurs, the loan term will be recalculated.

When can a borrower be recognized as a fraudster?

Using the statute of limitations in order to avoid repaying loan funds can result in unpleasant consequences for a person. That is, in addition to sending a statement of claim to the judicial authorities, the bank can contact law enforcement agencies in order to initiate a criminal case against the borrower under Art. 159 of the Criminal Code of the Russian Federation “Fraud”. In this case, an unscrupulous bank client may find himself in a more difficult situation than expected.

In order to avoid such consequences, the borrower is required to send a notice to the financial institution of temporary insolvency to repay the debt.

Also, evidence that the citizen did not have malicious intent can be:

- Making mandatory loan payments (at least several).

- Availability of movable and immovable property that was provided as collateral.

- If a small loan amount is not repaid.

It is important to know that if the debt collection period is missed, then the creditor does not have the right to pursue the citizen through the court under Art. 159 of the Criminal Code of the Russian Federation “Fraud”.

Debt collection using debt collectors

Often, after the collection period has expired, some banks may forget about the unscrupulous client by selling his debt to collection companies. Accordingly, collectors will demand the debt from the borrower. In addition, the amount of surcharge provided by collectors can start from 50% to 200–300% of the original volume.

However, if the contract did not provide for the transfer of debt to third parties, then the citizen is not obliged to do anything. That is, he should not pay off any debts to private companies that specialize in collection.

But, nevertheless, if the debt was sold by a financial organization to collectors, a citizen can observe similar phenomena:

- Collectors visit the borrower’s place of work.

- Attempts to put pressure on neighbors to obtain funds.

- Regular calls throughout the day with insults or threats to the life and health of the debtor and his close relatives.

- Damage to property (breaking glass windows, writing on doors, etc.).

If a citizen is put under pressure in this way, then he can safely send a statement to the prosecutor’s office. In this case, both the collection company and the financial organization itself will be held accountable, since the rights of a citizen were violated (transfer of personal data to third parties, as well as interference in personal life).

Of course, it is possible to avoid repaying loan funds, however, such cases are an exception. In addition, financial organizations file lawsuits in court before the loan collection period expires. But even if a citizen managed to avoid debt, he may face such consequences as a bad credit history. Simply put, you can forget about getting a loan for 10–15 years. As for the bank to which the loan funds were not transferred, it puts the borrower on its black list, which has no statute of limitations.

If the borrower stops making payments at some point, the organization after a few months begins to take measures to repay the debt. But she does this only up to a certain point. for credit debt expires when the financial institution gives up attempts to return its funds. It lasts three years. This is how much time is given to the creditor to repay the debt. But at what point exactly does the countdown begin? And what are the consequences for the borrower of non-payment of loans?

Is the bank capable

A person's financial situation may suddenly deteriorate. There are many reasons for this: illness, loss of work or other circumstances. In such a situation, sensible people tend to limit their expenses. But what should a person do who, in more favorable times, managed to conclude one or more loan agreements, and the inability to fulfill obligations makes his life unbearable? For borrowers who have not improved for several years, there is a law according to which banks do not have the right to disturb him after a certain time after the last deposit of money into the loan account. Is the bank capable of forgetting about those who owe it?

Every borrower knows that the statute of limitations on credit debt is three years. However, for some reason, even among experts there is no consensus as to at what point the countdown should begin. In addition, almost every judicial institution tends to interpret the statute of limitations for credit debt (Civil Code, Art. 196) in its own way.

From what date should the countdown be made?

This question is quite controversial. First of all, you need to know that the starting point does not begin from the day the agreement is concluded with the bank. Many borrowers believe that the statute of limitations on credit debt should be counted from the date the loan was received. And this is the main misconception. Courts often rely on the condition that this period begins to run from the moment of the last transaction, that is, from the day the borrower made the last monthly loan payment. Decisions made by the Supreme Court and the Supreme Arbitration Court of the Russian Federation are often based on this position.

Another opinion

But in our country there are still many judicial institutions that express disagreement with such an interpretation. Referring to Art. 200 of the Civil Code, they argue that the statute of limitations for credit debt should be counted from the date on which the individual’s agreement with the bank ends. Therefore, based on this statement, if a borrower took out a loan for six years, but stopped paying on it a year after it was issued, only after eight years will the statute of limitations on the loan debt expire.

Appeal

It should be noted that not all courts are guided by this position. And the countdown occurs only in those court cases in which we are talking about debts on cash loans, because cards often have an unlimited term. But if for a person the law on the statute of limitations for credit debt has become the only way out of the current situation, and the court has taken an inconvenient position for him, you can always count on an appeal.

It is the court that sets the statute of limitations, but in doing this, it takes into account all the relations between the borrower and the bank that have taken place since the conclusion of the loan agreement. There are some nuances to keep in mind. If, during the term of the loan agreement, the debtor applied to the court with an application for restructuring or with another request, the implementation of which usually helps to alleviate the plight of a person unable to deposit funds into the account, this fact may stop the statute of limitations. Why is this happening? The fact is that, as a rule, any attempts to reach an agreement with the bank involve depositing at least a symbolic amount into the credit account. And even if this did not happen, in court even the very fact of contacting a financial institution can be perceived as the last payment, from which the countdown begins.

What does not affect the course of time?

It is worth noting that some actions of banks cannot in any way affect the establishment of the date from which this period begins. Such actions, for example, include resale of debt to collectors. Despite the articles of the Civil Code mentioned above, it is not easy to determine the date when the statute of limitations on a loan begins. Advice from a lawyer is perhaps the right step in resolving this issue. You should not rely on the recommendations of non-professionals, following which can only aggravate the debtor’s situation.

What happens when the statute of limitations has expired?

2015 is a difficult period for Russia economically. Several years before the start of the so-called crisis, banking organizations entered into loan agreements with their clients in large quantities. At the same time, the requirements for potential borrowers were low.

But the unstable economic situation in the country has led to a significant deterioration in the standard of living of most citizens. Unemployment increased and food prices rose. For many Russians, monthly loan payments have become an unbearable burden. The recent loyalty of banks towards their clients has resulted in a tremendous increase in loan debt. In these conditions, many borrowers hope for the notorious statute of limitations on credit debt. After the trial, they believe, all debts will be written off, and life can begin with a clean slate. However, such an opinion is a grave mistake.

The expiration of a three-year period, after which the bank stops demanding its money, only means that the debtor has a reliable argument. Subject to the lender's repeated appeal to the courts, the borrower can point to it. The expiration of the claim period does not deprive the bank of the right to call and remind about obligations. But even in such cases, a method of counteraction is provided for the debtor. It consists of an application for revocation of personal data.

Selling debt

After the bank loses hope of getting its money back, life can be far from easy for the debtor. Many financial institutions, as you know, prefer to communicate with employees of such organizations - not a pleasant thing. Even those who have never entered into a loan agreement know this. The illegal actions of these people are often talked about on television, written in newspapers and on Internet news sites.

Collectors cannot go to court after the expiration of the claim period, and their only remedy is moral pressure on the debtor. A person who has suffered from communication with such employees should immediately contact the police. If they do not respond in any way to an application filed on the basis of unlawful actions of collectors, do not despair. The next step should be to contact the prosecutor's office.

Abuse of borrower rights

The person who issues the loan is responsible for this. In recent years, non-payments have increased significantly. This is not only the fault of borrowers, but also of banks and even the state. However, in some cases, loan non-payment depends entirely on the bank client. Such cases may include personal circumstances or outright fraud. The borrower must know that if he takes out a loan and initially hopes for the opportunity not to repay it, which can be facilitated by the statute of limitations law, he risks incurring administrative and even criminal liability. The minimum punishment facing the debtor is the collection of property. But the legislation also provides for more stringent measures.

Criminal liability

If a bank client takes out a loan with collateral, he does not face criminal liability. In case of non-payment, everything goes under the hammer. Although there are concessions here too. The bank cannot sue the apartment and the debtor if it is the only real estate. The exception is cases when fraud is seen in the debtor's actions.

It is not so difficult to determine whether the borrower was guided by bad thoughts. If after applying for a loan he deliberately hides, this does not speak in his favor. Depending on the specific situation, the debtor may be sentenced to correctional labor and even imprisoned for up to three years. However, such criminal measures are applicable only if the fact of theft of bank funds is proven.

Practice shows that most have negative consequences for the borrower due to the lack of qualified defense in court. The lack of special knowledge and the inability to defend one’s rights before the creditor often lead to the fact that the court fully satisfies the bank’s demands. There are often cases when the court makes a decision in favor of the bank after the statute of limitations has expired. And all because the borrower did not know about its existence and could not declare it. What is the statute of limitations on a loan, and when does the bank lose the right to demand repayment of the debt?

The statute of limitations on a loan involves a certain period of time that is given to the lender to sue the borrower in order to collect the overdue debt. After this period, the debtor has every right not to repay the outdated loan, and the bank, in turn, will no longer be able to forcibly collect funds from its borrower.

According to the Civil Code, the statute of limitations for a loan is 3 years. The legislation provides for the possibility of increasing this period, but only by agreement of the parties. This means that only if the borrower personally signed the document extending the limitation period, the creditor has the right to demand collection of the debt. Trying to circumvent this rule of law, banks often resort to various tricks. They sue the borrower for outdated loans, citing the fact that the increase in the statute of limitations was specified in the “Basic Conditions” that were attached to the loan agreement. Such actions of banks were stopped by the Supreme Court of Ukraine, considering case No. 6-16tss15. According to his resolution, only the borrower’s personal signature on the relevant document can become the basis for consideration of the bank’s claims in court.

Another issue that causes a huge amount of controversy is the beginning of the reporting period of limitation. Banks often insist on counting the term from the expiration date of the loan agreement. It is much more profitable for debtors to start reporting from the date of the last loan payment. For a long time, the courts took a rather ambiguous approach to this problem. The Armed Forces of Ukraine again put an end to this issue when considering case No. 6-160tss14. Referring to Article 261 of the Civil Code, the Supreme Court indicated that the limitation period for a loan begins from the moment the right to claim arises. The bank has the right to deduct the limitation period in relation to each specific clause of the agreement, that is, each monthly payment according to the debt repayment schedule up to the date of fulfillment of the last obligation.

However, that's not all. There is also a so-called special statute of limitations for a loan, which limits the time the creditor can demand the collection of fines and penalties for overdue debt. This period is only 12 months. This means that after one year, the bank loses the right to sue the borrower for all fines and penalties accrued on the principal debt.

Therefore, the first thing you need to do when you receive a subpoena for a loan is to check the statute of limitations. If the statute of limitations on a loan or penalties has expired, you do not even need to file a counterclaim - you just need to write a written statement to the court. A qualified lawyer will help you correctly calculate the statute of limitations on your loan and deprive the bank of the opportunity to demand the recovery of any funds!

(8

ratings, on average: 5,00

out of 5)

(8

ratings, on average: 5,00

out of 5)

Let's talk about what it is statute of limitations on loan and how much is statute of limitations on a loan. I will say right away that there is no clear opinion on this issue. As you know, our legislation is such that it can often be interpreted in two ways, the same is observed in the case of claims for overdue loans. Let us consider all the most common interpretations of this concept in judicial practice.

What is the statute of limitations on a loan?

The statute of limitations on a loan is the period during which a lender can file a lawsuit against a borrower who has violated the loan agreement and has not fulfilled its obligations.

Judicial practice shows that different courts in the same situations take different positions regarding the limitation period for a loan, and therefore make different decisions.

First of all, it is worth saying that credit relations are regulated by the norms of the Civil Code. The statute of limitations on a loan, in most cases, is 3 years, as with any civil offense. However, there are nuances.

From what date should the statute of limitations for a loan be counted?

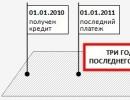

The main nuance is what date to count 3 years from. There are 2 main options here:

– From the end date of the loan agreement;

– From the date of the last payment.

This can be represented schematically as follows:

The second option is more profitable for the borrower-debtor, and the first option for the creditor bank.

In most cases, courts are still inclined to the second interpretation of the legislative norm, that is, the limitation period for a loan is counted from the date on which the borrower last repaid the debt or interest.

However, there are cases when, when considering a claim, the first interpretation is used - the limitation period for a loan is counted from the expiration date of the loan agreement. In any case, this option is not suitable if the established overdraft limit is valid on an indefinite basis.

But there is another option. The statute of limitations on a loan can be counted from the moment when the creditor learned about the formation of a problem debt and had the opportunity to begin the collection procedure. For example, this may be the first repayment date, on which and after which the borrower made no repayments at all. Some courts may also accept the following interpretation: everything depends on the judges, the bank’s lawyers and the debtor’s lawyers.

It is also important to know that the statute of limitations on a loan can be calculated taking into account official documents indicating negotiations on debt repayment between the bank and the borrower. For example, if the borrower contacted the bank with an application at the moment when he stopped repaying it, the date of receipt of the application may become a new date for starting the statute of limitations on the loan. And if the bank agreed to carry out a restructuring, and a corresponding agreement was signed, its date will definitely interrupt the limitation period and become the beginning of a new countdown.

It is also important to note that if the bank sells your debt to collectors, this does not interrupt the statute of limitations on the loan; it will continue to count from the moment the client stopped making payments.

There is one more point. The statute of limitations on a loan can be revised upward if the parties agree on this themselves. Therefore, recently, many banks and other credit organizations began to include in loan agreements a clause stating that the limitation period for this loan is not 3, but, for example, 5, 10 or even 50 years. Many borrowers, of course, do not read the agreement carefully, or do not read it at all, and do not pay any attention to this point. And only when it becomes difficult, litigation with the bank begins, they understand that if this period were shorter, there would be certain chances of avoiding repayment of the debt.

Can a bank demand repayment of a loan after the statute of limitations expires?

Typically, the debtor believes that if the statute of limitations on the loan has expired, then the bank or collectors no longer have the right to demand anything from him. However, it is not. They can still demand, and they can even file a lawsuit, except that they most likely will not win this court case. But the expired statute of limitations on the loan will not save you from calls, letters and other “harassments.”

In addition, the court itself does not calculate the limitation period for the loan itself. The debtor can present it as an argument in his favor - for this he needs to submit a corresponding petition to the court. On this basis alone, when considering the case, the judge will most likely refuse to satisfy the creditor’s claim if he considers the statute of limitations to have expired and the creditor does not find more compelling arguments in his favor.

The bank can also sell problematic debt with an expired loan statute of limitations to collectors who, realizing that they legally cannot present anything to the debtor, will probably begin to use illegal methods of influence against him, for example, threats or even worse.

Now you know what the statute of limitations on a loan is and how the statute of limitations can be calculated. Of course, it is necessary to understand that each case is individual. I tried to describe all the most common situations that I found in the comments of lawyers and attorneys.

In any case, I advise everyone to fulfill their loan obligations in a timely manner, to take loans only if you are confident in your ability to repay them, and also when it is in principle advisable (more about this in the article), so as to never let things go to waste. court and do not hide while waiting for the expiration of the statute of limitations on the loan.

Hello, please tell me. The court decision in the case was made in June 2013 on the collection of debt, at the end of 2017 no one made a deduction. The bailiffs allegedly lost the decree. Now they have started to withhold the amount. Has the statute of limitations passed? Can I apply for termination retention due to expiration of the statute of limitations

Hello. As far as I know, the execution of a court decision is also given a three-year period. But deductions can be made longer, until the debt is repaid. Try to consult with a lawyer on this issue, and if this is possible, of course, apply.

Hello! please tell me with a question! a consumer loan (mobile phone) was taken out in 2012, the last payment was made, in 2018 a call was received from Privat Bank about the debt on the loan and a fine in the amount of 5900 UAH. which I must close within 2 days, saying that I’m sorry, so much time has passed, where did the debt come from? answer: the collection period under the contract is 50 years. and you must close the debt or the security service will communicate with me! people will also come home and describe the property! tell me what to do?

Hello, Sergey.

If you still owe the bank, the debt cannot “disappear” anywhere, and fines are accrued according to the agreement. If they are provided for in tariffs, the bank has every right to charge them. If the contract specifies such a collection period, then that is what it is. But only bailiffs have the right to describe property by court decision. What should I do? Start by reading the terms of the loan agreement, check how valid the bank’s current requirements are. Suggest that the bank sue. If they do, file a claim there about the expiration of the statute of limitations. If the contract does not stipulate a different period (for example, 50 years, as they say, or some other term), then it is 3 years. In this case, the court will most likely take your side. And you will still communicate with the security service and collectors until the debt is closed. If you don’t want to repay it, make sure that they don’t break the laws or take illegal measures. If there are any, record them and file a statement with the police.

Good afternoon In 2001, I took out a phone on credit from a private bank, the price was 1500 UAH. There was no way to pay. The collectors began to bother me. In 2006, part of the loan was repaid. Three months ago I went to a private bank to apply for a card for social payments (I am disabled 3 grams). They asked me to activate the card by putting a small amount on it, I put 20 grams. After which they wrote off 9 grams to the account debt repayment! The next day, threatening calls began, and they persistently explained that I had to pay off a debt of 84,000 grams or confiscation! Today I received an SMS that inspectors came to me to describe the property (at my place of registration). I have not lived at the address where I am registered for about 7-8 years, there is no property there either! There is also no way to pay off the loan since I live on benefits! I forgot to say when they called and asked to pay the loan, I said that I could repay the loan without accrued interest (1500 UAH), but they rudely told me that I owed 84,000 UAH, and I would pay everything! Tell me what actions to expect from the bank? And what should I do in my situation, what should I be afraid of?

Hello, Sergey. Yes, the actions will be approximately the same as they are. You yourself are to blame for this, because... did not repay the loan on time. You cannot take out loans without being 100% sure of their repayment. Moreover, a telephone is far from an essential thing. Officially, they are unlikely to be able to take anything from you (only bailiffs can do this, and the court is unlikely to do so). That’s why they will bother you and intimidate you like this. If the bank still has the debt, then most likely in the future it will be sold to collectors, and you will communicate with them. You make sure that they don’t break the laws at least.

Hello, please tell me how to solve this problem, I took out a loan from moneyveo for 3000 UAH. I had to return 3009 UAH. Before taking the loan I called the manager and asked what interest would be accrued after the first prolongation, to which I was told that after the first prolongation no interest is calculated only after the second 10% of the loan amount, I made an extension, literally 3 days later I was credited 740 UAH, in the process I was unable to pay the amount, the delay is very long, about 5 months, the amount at the moment is 14690 UAH, the debt was sold to another company

Hello, Vitaly. What some manager told you doesn't matter. What is paramount is what is specified in the loan agreement. Have you read it? But in general, the essence of the question is for you here:

Hello, please tell me what to do if the loan was taken using a stolen passport. The passport was stolen in 2008 and the loan was taken in 2016. At the moment, the bank has already closed the loan and sold it to the collector; they send threatening letters every month, asking you to respond.

Hello, Nikolay. It was necessary to write a statement to the police about the theft of the passport, and now provide the collectors with a copy of this statement and some kind of response from the police. That is, to confirm that you have not used this passport for a long time and it was actually stolen a long time ago, it is no longer yours. You can also provide your new passport with the date of issue of a previously received loan as proof and write a letter to the collectors that you have been living on this document for a long time, and it was stolen, attaching official documents from the police about this.

Good afternoon Help in this situation - in 2012 I took out a loan from OTP Bank, they didn’t give me a copy of the contract right away, explaining that there was no stamp and I could pick it up either the next day or during the next payment. Neither the next day nor during the next payment the agreement was ready, and so on for 3 months in a row, I decided to take out a loan from another bank, and repaid it at OTP Bank and asked for a certificate of closure of the loan, but again they gave me the excuse that there is no stamp now, well and God bless them, I thought, the main thing is that I don’t owe them anything. So this year (02.17) an alleged bailiff called me and told me that the bank had filed a lawsuit against me and I had to pay the menu by today, I don’t know what to do, there is no contract, I don’t know the payment in 6 years and where, he threatened to come and to evict from the house, although when the loan was taken out the apartment was not collateral and I have not lived there for 5 years. What to do?

Hello, Vera. I doubt that the bailiff called you. No one will evict you without a court decision. But in this situation, they themselves are to blame - they should have demanded an agreement and/or a certificate in writing. First, collect all the documents on repayment; it’s good if they have been preserved. And also request (in writing!) from the bank a copy of the agreement and calculation of the debt. In the letter, describe in detail the whole situation, that they assured you that the loan was repaid (who, how, when), and each time they refused to give up the agreement. Demand an explanation of the situation.

Hello Konstantin. I have the same problem. I took out a loan in 2008, and it so happened that I didn’t pay it off. There were no letters until 2018. And recently I received a letter saying that your debt is 19,000 thousand. According to a court decision, if within 7 days If the debt is not paid, the bailiffs will come to describe the property. I was discharged where I lived, also somewhere in 2009. What should I do? I am in another country. I have been for about 8 years now. And my sister remains there.

Hello, Evgeniy. Debts need to be repaid - this is logical. But the question is - what kind of letter is it, who is it from? It is very likely that there was no trial, and the collection company that bought your problem debt is simply misleading. To write “according to a court decision,” you first need to see this decision.

Tell me what to do My son took out a credit card for the amount of 2500 UAH from Privat Bank on 05/24/2011 on 12/03/2017 he was counted 18,000 UAH and the court awarded Privat Bank but he was not summoned to court while the bank is deducting his son from his salary and the bank calculates new interest, what can be done ?

Hello Irina. You need to pay what the court has awarded. Because debts must be repaid and the terms of contracts must be fulfilled. You could have filed an appeal within 10 days, but apparently you didn’t have time.

They can submit it. And if you find out about this, file a statement there about the expiration of the statute of limitations.

I haven’t deposited money on a credit card for 3 years, but the card has an expiration date until 2016. Can the bank sue me after 3 years from the last payment? Please tell me briefly what to do?

Of course it can. Nothing depends on the expiration date of the card; it depends on the terms of the loan agreement. What to do... depending on what is happening. In general, you need to fulfill your obligations.

Good afternoon. A question. My Privatbank credit card was overdue. It was not possible to pay because due to personal circumstances I had to leave the country for an unknown time. I have not been in the country for more than 5 years. I have no property. There is a registration. All letters arriving at the place of registration are returned to the sender. During all this time, interest is accrued on late payments. The amount is no longer small. I will not return to the country anymore. What can the bank do in this case? So what should I do?

Hello, Alexander. You need to fulfill your obligations - this is logical. The bank cannot do anything for you personally in this situation. Most likely, he will sell the debt to collectors, and they will begin to harass your relatives. It's illegal, but I think that's how it will happen.

Good afternoon Tell me, is it possible to go through the trial without my participation? I received this SMS:

By decision of the court, on June 08, 2018, a forced entry into your home will take place to inventory your property with a police representative. Lawyer Shvidko Zaima. Only 2 months overdue. I did not receive any letter about the trial. How should I proceed? I didn't refuse to pay. Due to family circumstances, it was not possible to pay on time. I warned you over the phone. I asked for a delay. I only received a rude refusal. Can they show up? I am only registered at the address indicated and do not live.

Hello, Snezhana. It is possible, for example, if you were sent a summons to court, but you did not receive it. But in this context, it is 99% that there was no trial. Courts do not send SMS messages. All deferments must be requested formally = in writing and with reason, no words mean anything. Only a bailiff with a real court decision in hand has the right to describe property. Everyone else who comes does not need to be let in at all. If they break in, call the police.

Good afternoon, my husband, when he was studying at school 7 years ago, opened a card in a private bank, he asked for a regular card so that his dad would transfer money to him, they swindled him into a credit card with a limit of 100 UAH, which he did not take, for example, his dad sent him 1230 rubles, he withdrew 1200.30 rubles remained, in general! Yesterday we received a letter saying that the debt is 38,000 UAH, and they are filing a lawsuit, damn... well, it’s fraud!!! The card has been invalid for two years already! 2013, but at the end of 2014 there was some receipt on the card in the amount of 11 UAH, and my husband was in Russia at that time and did not use the card, I suspect that the bank insured itself in such a way that it would extend the period of three years when the debt is cancelled, and now they have filed a lawsuit when the card has been invalid for two years, and there is a month left until 3 years when the debt can be written off, what should we do???

There is a loan, there is debt restructuring, but the loan is overdue for 2 years 10 months, there were 10 thousand left 4256, I received an SMS saying that “we know your property is important to you” “” “call back to 3700, I dialed, the girl operator said pay 1200 at least before 18.06 if not, the bank will sue. Tell me if they really apply for such amounts

It is difficult for me to judge the debt collection policy of a particular bank. But if they do, it’s better for you, you won’t lose anything from it. Debts still need to be repaid, but they won’t award you any extra money. Important: do not agree to any verbal agreements like “pay at least 1200”. If so, then only after concluding a written agreement to this effect.

Good afternoon, dear Konstantin!

Could you help me find an answer or give me advice on the following question:

I received a summons to court with a debt of 3100 UAH. on loan, 1300 UAH. on foam and!!! 112000 UAH. (x40 from the body)

The last payments are clearly not mine (I know for sure that I didn’t pay them)

– 3200 UAH. 03/04/2013 (at that time my entire salary, and I clearly don’t remember living without money for a month)

– 1 UAH. 02/03/2014 (well, this is funny)

– 700 UAH. 07/12/2015 (my daughter was just born, I physically couldn’t do it and why would I do it if I hadn’t paid for 2 years)

Apparently my last payment was on January 22, 2013.

What to do if the bank itself “drew” the transactions on the accounts so that there was a statute of limitations?

Does it matter to the court whether the payment actually took place and who made it?

Should I (or on my behalf/interest) be the one who performed the transaction?

Doesn’t the court care that since 2013, it wasn’t me who paid only 701 UAH, and the bank just now filed a lawsuit?

Can I demand evidence from the Bank at a court hearing regarding payments that I did not make?

Thank you in advance

Sincerely,

Eugene.

Hello, Evgeniy.

I am not a lawyer and I don’t know the legal intricacies of participating in courts, I can only speak from a financial point of view; to clarify the legal nuances, it is better for you to contact a lawyer. I'll write what I can say.

If the bank “drew” account transactions, naturally, you need to prove that you did not make these payments. In this case, there should be your signatures on the payment documents (but they are clearly not there or they are fake), and in general, most likely, such “drawing” took place retroactively, now, before the court. This means that there are definitely inconsistencies in the bank’s consolidated financial documents for those days. And if you raise all this, it will probably be revealed. Therefore, if you are sure that you did not do this, prove it in court. Demand that the bank provide the relevant payment documents and daily reports (cash or non-cash), which should include these documents. They are not easy to fake.

And now file a petition with the court about the expiration of the statute of limitations (if you don’t file it, it won’t take it into account).

The transactions did not have to be carried out by you – anyone could repay the loan for you.

The court considers the documents that are provided. Of course, ask for proof.

Good afternoon. Question: I have an agreement with Mikhailovsky Bank. Compiled in 2015. Can I sue to cancel this loan agreement based on expiration? (Last payment was made more than 3 years ago)

Hello, Pavel. Of course not. The agreement is valid until the parties fulfill their obligations or a certain period specified in the agreement.

Good afternoon. Today I contacted Privat Bank to open a card and found out that in 2008 a fine of 200 UAH was charged on a credit card, which I did not know about to this day. I was sure that the credit limit had been repaid. And today the amount of debt is 10,000 UAH. Moreover, all these years there was not a single call, not a single letter from Privat Bank.

A bank employee offered to reissue this card so that I could start paying off the debt. What to do in this case?

Hello, Victoria. If you don’t want to pay off this debt, don’t use the services of this bank anymore. Invite them to sue if there are any complaints.

Good evening. Such a situation, the private company sued for late payment of the loan, but, having submitted to the court an agreement on issuing a debit card and not a universal one. Tell me, what is the probability of fighting off the bank and changing your credit history? Thank you in advance.

Hello, Vladimir. You need to protect your interests in court. Especially if you believe that the bank is being cunning and doing something wrong. But the credit history does not change in any way.

Hello, tell me how to behave in this situation!

I took out a loan in January 2014 from Oschad Bank and paid regularly. But in July 2014, the war, or rather the ATO, began in the city where I live. The banks closed, I left the ATO zone and continued to pay the loan until February 2015. Then she returned to her hometown and did not pay the loan because... banks in the non-controlled territory of Ukraine stopped their work. And today the executive service called not me but the guarantor, allegedly his property will be seized, but he is also in the ATO zone. How are things going now with the collection of debt from citizens living in uncontrolled territory? What to do and what threatens the guarantor?

Hello, Ekaterina. In 2014, the Law “On temporary measures for the period of the ATO” came into force in Ukraine. According to it, banks do not have the right to charge interest and fines to borrowers living in the ATO zone. However, the principal debt remains in any case, and banks have the right to demand its repayment. If there is a court decision to collect the debt, then the debtor and the guarantor have the right to seize the property, incl. in uncontrolled territory. But in fact they will not be able to do anything with this property. And yet, there is a statute of limitations, which for debts and loans is 3 years, usually counted from the date of the last payment. Therefore, if the court has now made such a decision, you can file an appeal or sue the bank again, arguing that the statute of limitations has expired. There is also a high probability that the call is not from the executive service, but from collectors to whom the bank sold the problem debt. And they are simply frightening. You need to see the documents and not believe anything you say on the phone. Well, the debt, of course, must be repaid, with interest accrued at the time the above law came into force, no more.

Good afternoon Tell me this situation, there was a private bank card! I closed it around 2012. They cut it in the jar and that’s it! Then in 2016 they called from the bank and said you had a debt of 22,000 gon, to which I replied that I closed the card and this was some kind of mistake, and I’m not going to pay them! They again fell silent and didn’t say anything, now today I received a letter to work with decree that I have a debt in a private bank of 58,000 and they will withdraw 20% from my salary?! What should I do?! thanks

Hello, Taras. “Cutting a card” does not mean closing an account. It’s the same as if you threw the plastic itself in the trash - that wouldn’t close the account. Read here: If there is already a court decision and the appeal period has expired, then you won’t do anything - they will just take 20% off your salary. If you are sure that the decision was made illegally, you can only file a counterclaim by spending money on lawyers, or by yourself thoroughly studying the legal aspects on this issue.

Hello! Half a year ago my loan in Maniveo was sold to DOVIRA AND GARANTIA. A week later they called me and told me to return the money. I returned 5,000 and sent them a photo of the receipt on Viber. And they wrote to me that I transferred the money to the wrong place. Although they sent the details! What to do? Have I been scammed?

Hello, Yuri. You need to be guided by official documents. For example, a letter with a signature and seal. The “discarded” details are not an official document. In addition, you should initially request a copy of the factoring (sale) agreement for your debt to make sure that it was sold at all.

Hello, a year ago I took out a loan from a cafe for 600 UAH, but I couldn’t pay it back because there were problems. Today, a year later, they call me, they say that the police have written a complaint against me and they want to open a criminal case, they threaten fraud and demand to pay off the debt in the amount of 12,000 UAH. I don’t have that kind of money, I’m on maternity leave. Tell me what to do? And can they open a criminal case?

Hello Anna. They are calling you not from the police, but from a collection company. There is no fraud here, unless, for example, you forged documents to get a loan. And if you think that you can take money and not give it back, I will disappoint you: this is not so. By taking out a loan, you are required to fulfill the terms and conditions that you signed. Read them carefully first to determine the size of your actual debt at the moment and think about how to close it.

Hello. My mother died in May 2018. After it, I was left with a share in the apartment, which I registered for myself in November, and a bunch of loans. Everyone has a 3 year term. The lawyers advised me to wait a little longer and not pick up the documents for the apartment for as long as possible. But everyone at home was already tired of saying that the documents needed to be picked up. One bank called and they know that mom is gone. But not one of the banks has filed a lawsuit in 3 years. What is the best way to proceed in this situation.

Hello, Klava. I am not a lawyer, and from a legal point of view I will not give you an exact answer. But if you have entered into an inheritance, the debts will also be inherited by you. Regardless of when you pick up the documents.

We took out a loan from the bank to buy a car in 2008. We paid until 2010, then because of the finances. the crisis was not paid for. The loan was taken out from Nadra (the bank is now in the process of liquidation). In 2017 there was an opportunity to pay. started paying. To date, we have paid off the loan in full. But the liquidation commission has changed and they require us to pay more interest for previous years. about 80,000 UAH. How can we get documents for the car and not pay off the debt that they are again imposing on us.

Hello, Marina. In your opinion, is it possible to “not pay the loan due to the crisis” and then say that a debt is being imposed on you?). This is wrong. Is it possible to take out a loan and pay off only the body without paying interest? This is also not true. Moreover, you could repay the loan in full if you had a standard repayment scheme, the loan and interest were paid to different accounts (this was the case a long time ago, but in 2008 this is not a fact). If you had an annuity repayment scheme or repayments went to one account (most likely), the loan body could not be repaid before interest, fines, penalties, because there is a repayment order (the body comes last when the rest is paid). You can try to sue the liquidators if you think you are right. You don’t have to pay for 3 years to allow the statute of limitations to pass, and then sue. To begin with, I would recommend taking some kind of official decryption of the debt and see what will be indicated there.

I took out a loan in 2010 from Ukrsotsbank, first 2000 then 7500. The loan was imposed on a salary card, I paid until 2014, the last payment was February 2015. They sold the debt to collectors. Will they sue?

How do I know what's on their mind? Most likely no. If they do, file a claim that the statute of limitations has expired.

PS: they cannot force you to use a loan.